GTS News Center & Latest Updates

Your Most Professional Enterprise Systems and Software Custom Development Provider!

GTS News Center & Latest Updates

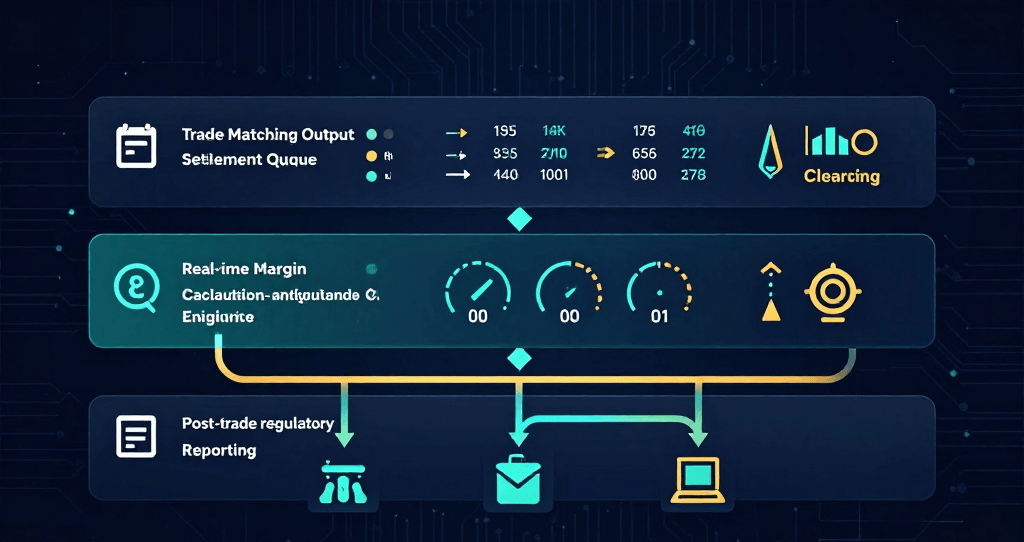

For technology decision-makers at Hong Kong financial institutions, trading system development has never been a purely engineering concern. Whether a system can handle concurrent multi-asset trading, meet regulatory technical requirements, and remain stable as business scales — the answers to these questions directly determine an institution's competitive position in the market. This article works through the core issues that enterprises must clarify when building a financial trading system, from order management architecture and clearing and settlement design, to engineering choices for low-latency systems. Before examining architectural details, it is worth first understanding Hong Kong's current regulatory context. The Securities and Futures Commission (SFC) authorises Automated Trading Services (ATS) under Part III of the Securities and Futures Ordinance (SFO), and requires relevant institutions to meet defined standards in areas including system capacity planning, stress testing, and abnormal trading surveillance — all of which are addressed in the SFC's Guidelines for Regulation of Automated Trading Services. In parallel, the Hong Kong Monetary Authority (HKMA) Supervisory Policy Manual module TM-G-1 (General Principles for Technology Risk Management) sets clear expectations for financial institutions regarding system development lifecycle management, change control, and disaster recovery planning. The practical implication of these requirements is this: compliance capability must be built into the architecture from the outset, not retrofitted later. Institutions that overlook the technical compliance foundation at the early stages of system development frequently encounter far greater costs when they reach the licensing application or regulatory review stage. When planning financial trading infrastructure, many institutions underestimate the pivotal role of the Order Management System (OMS) within the overall architecture. An OMS is not simply an "order recording tool" — it is the core coordination layer connecting the quoting engine, pre-trade risk validation, matching engine, and clearing and settlement. A well-designed OMS must be capable of handling several categories of critical business logic: Order Routing and Execution Strategy: When operating across different markets — Hong Kong equities, US equities, derivatives, and virtual assets — the routing rules, partial fill handling logic, and market connectivity protocols each differ. The OMS must support flexible multi-asset, multi-market configuration through a unified interface, rather than relying on multiple isolated systems maintained in parallel. Pre-Trade Risk Embedding: Effective risk control does not intervene after matching — it validates before orders enter the matching engine. The OMS must have built-in position limits, capital adequacy checks, and abnormal order interception mechanisms, ensuring every order is already compliant with the institution's defined risk parameters before it reaches the market. Audit Trail Completeness: From order creation, amendment, and rejection through to final execution, the OMS should record timestamps at every status node. This supports regulatory compliance requirements for transaction traceability and provides a reliable data foundation for internal audit purposes. For a deeper look at how the matching engine and risk modules are co-designed within an enterprise architecture, readers may wish to refer to our earlier article, Securities Trading System Customisation: “Custom Securities Trading System Development: From Matching Engine to Risk and Clearing Integration”, and is well-suited for technical leads currently conducting system architecture evaluations. Clearing and settlement is frequently the most underestimated component in financial trading system development. Many institutions assume that connecting to CCASS or OTC Clear completes their post-trade processing requirements. In practice, a broker-level clearing intermediate layer is a distinct and necessary engineering project in its own right. In Hong Kong's market environment, an institution's self-built clearing layer typically needs to cover the following functional modules: DvP (Delivery versus Payment) Logic: This ensures securities and funds are exchanged simultaneously, eliminating the settlement risk that arises from one-sided failures. Within the T+2 settlement cycle, the system must track the status of every pending settlement in real time, and trigger predefined exception-handling flows upon settlement failure. Margin Calculation Engine: For businesses involving derivatives or leveraged trading, the system must calculate each account's margin level in real time and automatically initiate margin call notifications or forced liquidation procedures when threshold levels are reached. The accuracy and real-time performance of this component directly affects the institution's ability to manage credit risk exposure. Regulatory Reporting Interface: The clearing system must provide standardised data output interfaces to support periodic filings and real-time reporting requirements submitted to HKEX, the SFC, or the HKMA — removing any reliance on the fragile practice of manually exporting compliance reports. Low latency is not a universal requirement, but for institutions engaged in algorithmic trading, quantitative strategy execution, or cross-market arbitrage, differences at the microsecond level translate directly into strategy profitability. When planning a low-latency trading system architecture, the following engineering decisions are among the most consequential: Co-location Strategy: Deploying the core execution nodes of the trading system within the same data centre facility as the exchange is the most direct and effective means of reducing round-trip network latency. Hong Kong Exchanges and Clearing (HKEX) offers co-location services that allow institutions to deploy servers directly alongside HKEX's own infrastructure, enabling round-trip latency to be held within single-digit millisecond ranges. Event-Driven Architecture vs. Polling: For scenarios such as order status updates and market data consumption, an event-driven architecture can significantly reduce unnecessary CPU utilisation and response latency. By contrast, polling introduces additional timing jitter under high-frequency conditions and is not suited to latency-sensitive trading paths. Kernel Bypass Technology: In extreme low-latency scenarios, bypassing the operating system kernel for network I/O — through technologies such as DPDK or RDMA — can eliminate tens to hundreds of microseconds of system call overhead. Implementing such technologies requires deep expertise in the underlying network stack and is generally not advisable for non-specialist teams to attempt independently. It is also worth noting that "low latency" and "high-frequency trading (HFT)" carry meaningfully different engineering requirements. When planning quantitative trading system infrastructure, institutions should first establish the execution frequency and order flow characteristics of their strategies, then select the appropriate technical approach accordingly — avoiding the trap of applying HFT-level engineering complexity to support mid-to-low frequency strategies that in practice only require millisecond-level responsiveness. Throughout the construction of all the modules described above, development efficiency and system reliability are equally important dimensions for enterprise decision-makers to weigh. GTS has integrated AI-assisted development capabilities into the delivery process for enterprise-grade trading systems — spanning requirements analysis, automated generation of architecture documentation, code review, and intelligent test case coverage. The introduction of AI tooling allows the development cycle for complex financial systems to be shortened by approximately 30% to 40%, while maintaining the documentation completeness and traceability standards required by Hong Kong's financial regulatory environment. This AI-efficiency-driven development model is particularly valuable for institutions needing to rapidly deploy new business lines — such as virtual asset trading or cross-border derivatives clearing — enabling enterprises to achieve a more competitive market entry window without compromising system quality. Is your institution's trading system ready for the next phase of business growth? Whether you are at the early stage of system evaluation or already have a defined module upgrade plan, GTS's technical advisory team can provide customised consulting and system design tailored to the Hong Kong market. Submit your requirements and we will arrange a dedicated technical discussion within two business days. Fully considered, trading system development is never a matter of assembling isolated modules — it is the organic integration of order management, clearing and settlement, low-latency execution, and compliance architecture. In a financial centre as regulatory-precise and competitively concentrated as Hong Kong, every architectural decision deserves careful scrutiny before implementation.

1. How Regulatory Upgrades Are Redefining the Baseline for System Development

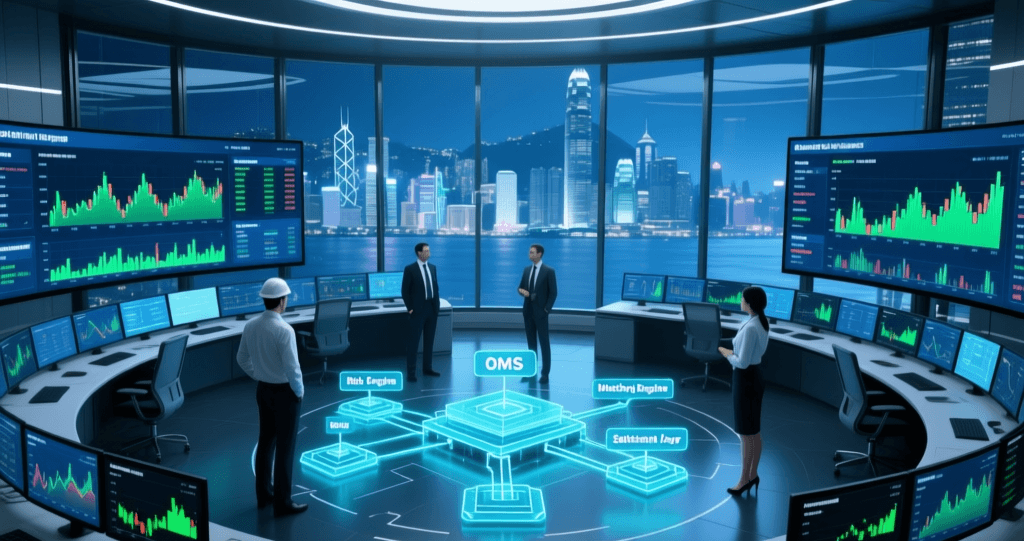

2. Order Management System: The Central Nervous System of the Trading Chain

3. Clearing and Settlement System: Key Design Considerations for Broker-Side Intermediate Layers

4. Low-Latency Trading System: The Architecture Decisions That Define the Boundaries of Competitive Advantage

5. AI-Assisted Development: How GTS Shortens the Delivery Cycle for Enterprise Trading Systems